✈️ I'm currently travelling overseas until 18/7/26. I'm still checking enquiries during this time, though response times may be a little slower than usual. Thanks for your understanding.

Split loan calculator

A split home loan combines the flexibility of a variable rate loan with the certainty of a fixed rate loan. Instead of choosing one or the other, you divide your mortgage into separate portions – typically fixing part of the balance while keeping the remainder variable.

Our split loan calculator helps you estimate repayments and compare how different loan structures may affect your monthly budget and long-term interest costs.

Whether you’re a first home buyer, refinancing an existing mortgage, or managing an investment property, understanding how split loans work can help you balance repayment certainty with flexibility.

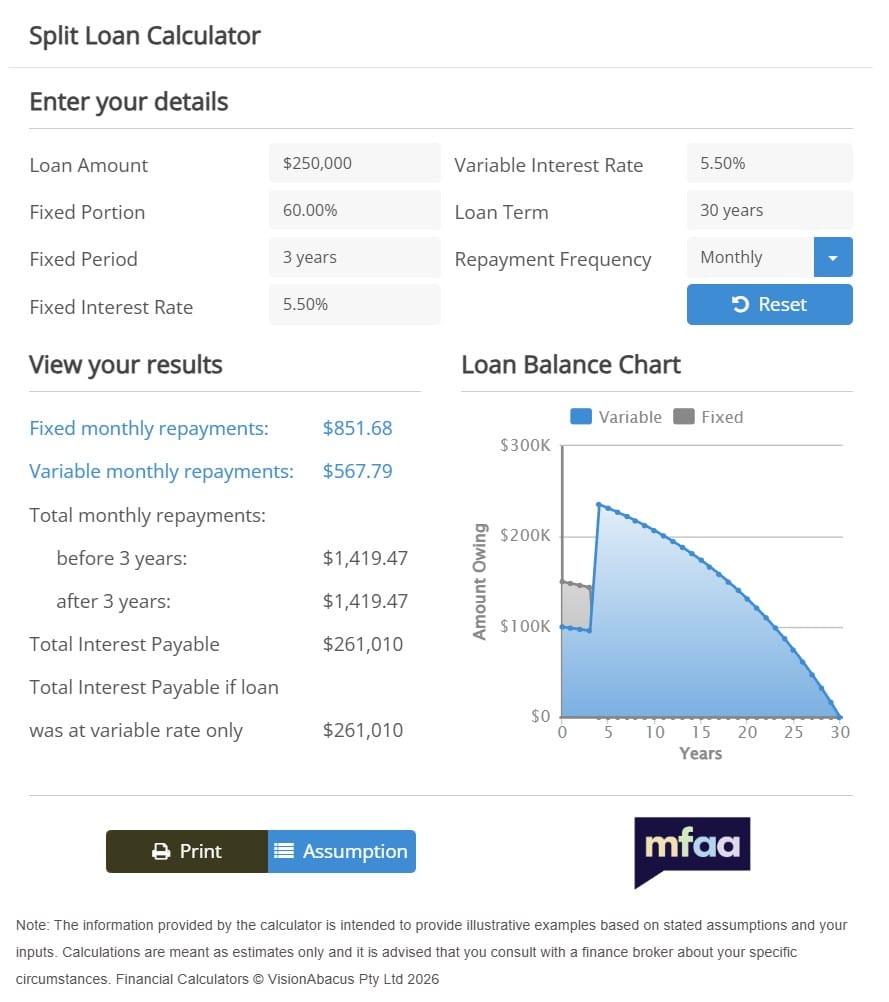

Compare repayments for fixed and variable rates

If you choose to fix your loan at a set rate for a certain period of time you will expect your repayments to change when your loan moves to the variable rate period. This calculator will help you understand how the repayments will change over time. To understand the loan options available including rates and features, give me a call.

Click on the Get Started button to get started with an application online or submit your question in the form below and one of our mortgage brokers will get back to you as soon as possible.

Interactive Calculator

Split Loan Calculator

Allows you to see your repayments between 2 fixed and variable loan amounts

Launch Calculator

How Does a Split Home Loan Work?

With a split home loan, your mortgage is divided into separate portions that may have different interest rates and features. The most common structure involves splitting the loan between fixed and variable rates.

For example, if you borrow $800,000, you may decide to:

- fix $500,000 for a set term

- keep $300,000 on a variable rate

The fixed portion of the loan provides repayment certainty for the agreed term, while the variable portion may offer greater flexibility and access to features like offset accounts or unlimited additional repayments.

Some lenders also allow borrowers to create multiple splits across a single mortgage. This may allow borrowers to stagger fixed rate expiry dates or structure their loan around changing financial goals.

Why Borrowers Choose Split Loans

Split home loans are popular because they combine some of the advantages of both fixed and variable loans.

Potential benefits of a split loan may include:

- greater repayment certainty on the fixed portion

- flexibility on the variable portion

- access to offset accounts

- the ability to make additional repayments

- reduced exposure to interest rate increases

- easier household budgeting

Many borrowers use split loans when they want to manage risk without giving up all the flexibility associated with variable rate lending.

Fixed vs Variable vs Split Loans

Choosing between a fixed, variable, or split loan depends on your financial goals, cash flow requirements, and comfort with changing interest rates.

Fixed rate loans provide certainty because repayments remain the same during the fixed period. However, they may come with restrictions on extra repayments, refinancing, or exiting the loan early.

Variable rate loans can increase or decrease over time depending on market conditions and lender pricing changes. While repayments may fluctuate, borrowers often gain access to features such as offset accounts and redraw facilities.

Split loans sit somewhere in between. They allow borrowers to secure certainty on part of the loan while still retaining flexibility on the remaining balance.

When a Split Loan May Make Sense

A split loan may suit borrowers who want a combination of stability and flexibility.

This type of loan structure is commonly considered by:

- first home buyers wanting predictable repayments

- borrowers concerned about future rate rises

- families managing tight household budgets

- investors wanting stable cash flow

- homeowners planning renovations or future expenses

- borrowers with savings held in an offset account

Because every borrower’s circumstances are different, the right split ratio will depend on your financial goals, risk tolerance, and future plans.

Potential Downsides of Split Loans

While split loans can offer flexibility, they may also come with some disadvantages.

The fixed portion of the loan may include break costs if you refinance, repay the loan early, or make changes during the fixed term. Some fixed loans also limit how much extra you can repay each year.

Managing multiple loan portions can also make the loan structure more complex, particularly if different interest rates or expiry dates apply across each split.

Before choosing a split loan, it is important to understand how each portion of the loan operates and what fees or restrictions may apply.

How to Use the Split Loan Calculator

Our split loan calculator allows you to estimate repayments based on different fixed and variable loan combinations.

To use the calculator:

- enter your total loan amount

- choose how much of the loan you would like fixed or variable

- enter the relevant interest rates

- select your loan term

- compare estimated repayments

You can adjust the split percentages to see how different loan structures may affect your monthly repayments and long-term interest costs.

Example Split Loan Scenario

Sarah and James are purchasing a home and borrowing $900,000. They want some repayment certainty but also want access to an offset account for their savings.

They decide to:

- fix $500,000 of the loan for 3 years

- keep $400,000 on a variable rate linked to an offset account

This structure gives them predictable repayments on most of the mortgage while still allowing them to reduce interest costs using their savings.

As interest rates and financial goals change over time, borrowers may review and adjust their loan structure when fixed periods expire.

Can You Have an Offset Account With a Split Loan?

In many cases, borrowers can still use an offset account with a split loan. However, offset accounts are typically linked only to the variable portion of the mortgage.

This allows borrowers to reduce the interest charged on the variable balance while keeping the fixed portion separate.

Loan features can vary between lenders, so it is important to compare how different split loan products operate and which features are available.

Is a Split Loan Better Than Fixed or Variable?

There is no single loan structure that suits every borrower. A split loan may be beneficial for borrowers who want both repayment certainty and flexibility, but the right option will depend on your individual circumstances.

Some borrowers prefer the predictability of fully fixed repayments, while others prioritise the flexibility of a fully variable loan. A split loan can provide a middle ground by combining elements of both.

Before choosing a home loan structure, it can help to compare repayment scenarios, review future financial plans, and understand how interest rate changes may affect your budget.

Frequently Asked Questions

A split home loan divides your mortgage into separate portions, usually combining fixed and variable interest rates within the same loan.

Extra repayments are generally allowed on the variable portion of the loan. The fixed portion may have annual repayment limits depending on the lender.

Yes, split loans can usually be refinanced. However, break costs may apply if you refinance during a fixed rate period.

Some borrowers use split loans to reduce exposure to rising interest rates while still retaining flexibility on part of the mortgage.

Yes, split loans are commonly used for both owner occupied and investment properties.

Some lenders allow borrowers to divide their loan into multiple fixed and variable portions depending on their needs.

The fixed portion of the loan may attract break costs if changes are made during the fixed term.

Split loans may suit first home buyers who want a balance between repayment certainty and flexibility, although suitability depends on individual financial circumstances.

Need some help?

Not sure where to start? That’s exactly what we’re here for. Drop us a message and we will get back to you within one business day with clear, honest advice tailored to your situation.