✈️ I'm currently travelling overseas until 18/7/26. I'm still checking enquiries during this time, though response times may be a little slower than usual. Thanks for your understanding.

Home Loan Pre-Approval Australia – Know Your Borrowing Power

Home loan pre-approval is the most valuable step you can take before you start seriously searching for a property. It gives you a clear picture of how much a lender is willing to lend you. This is based on your current income, expenses, and financial situation. That means no guessing, no wasted inspections and no falling in love with a home that is out of reach. You can search with a realistic budget in mind from the start.

Pre-approval also puts you in a stronger position when you find a property you want. Sellers and agents take pre-approved buyers more seriously, and in competitive markets it can make the difference between securing a property and missing out.

Whether you are a first time home buyer, or looking for your next home or investment property, securing a pre-approval can help give you peace of mind as to what you can afford.

Use the borrowing power calculator below to get an initial estimate of your borrowing capacity. Keep in mind it’s a guide – every lender assesses applications differently, and your individual circumstances play a big role in the final figure. Once you have a number in mind, read through the six things worth knowing about pre-approvals before you apply, or get in touch and we’ll walk you through it.

One of the first things most people want to know is, what is my borrowing power. Without further ado, lets talk numbers:

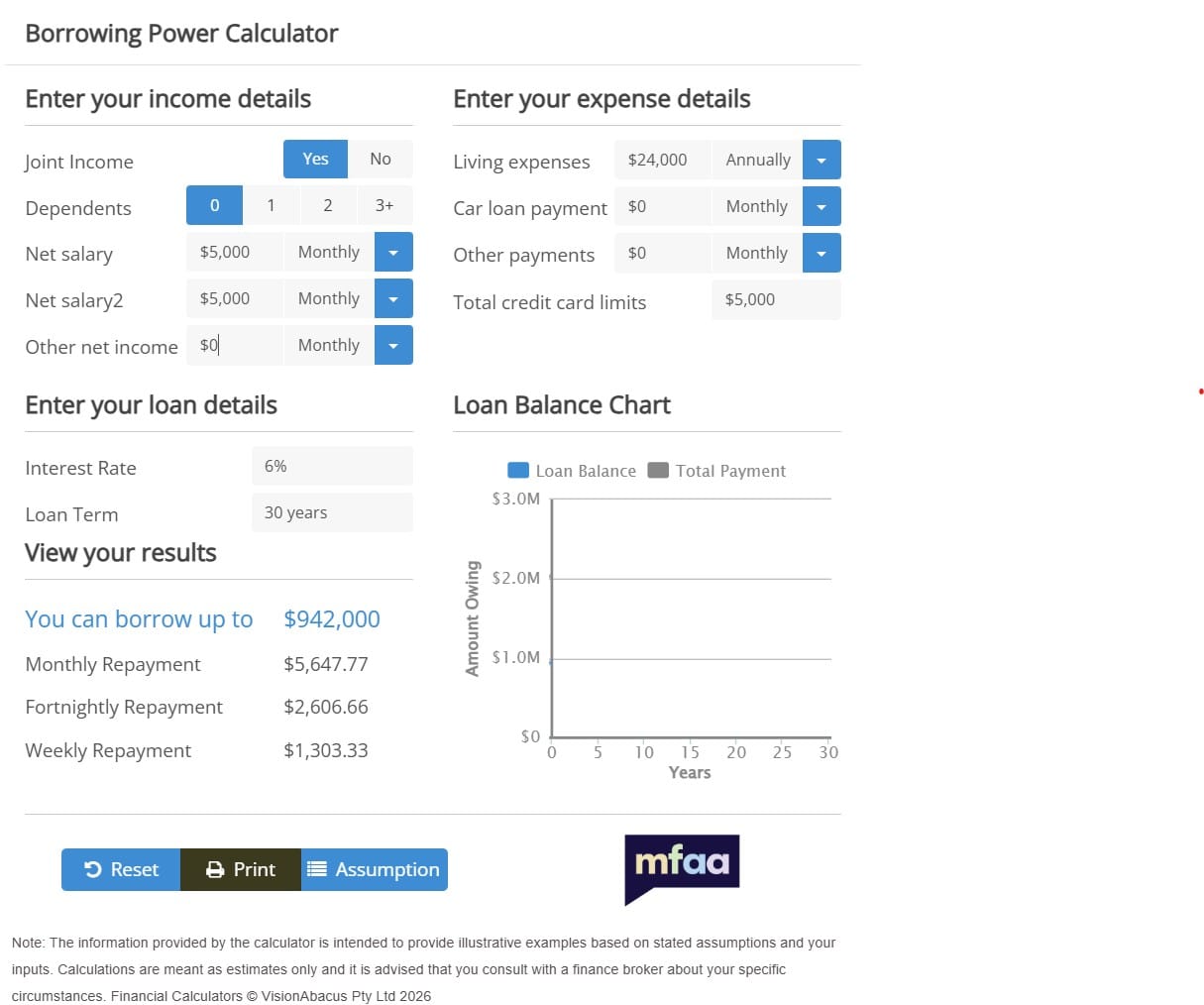

Interactive Calculator

Borrowing Power Calculator

Estimate how much you may be able to borrow based on your income, expenses and existing commitments.

Launch Calculator

The above calculator is only a guide and isn’t perfect. Each lender has their own criteria and of course each client I assist has their own individual circumstances too. Reach out so we can discuss your situation in more detail and confirm a more exact figure for your situation. Got other questions? We’re here to help.

6 things to know about pre-approvals

1. What is pre-approval?

A pre-approval indicates how much a lender may be willing to lend you based on your current financial situation. It is not a final loan approval, and you do not have to proceed with that lender. The lender also does not guarantee approval, especially if your circumstances change before settlement.. A pre-approval helps you narrow your property search, bid with greater confidence, and shows sellers that you’re a serious buyer.

2. How long is pre-approval for and what can I do if it is expiring?

In general, pre-approval can be around two or three months, depending on your lender. Your pre-approval paperwork will outline the expiry date of your pre-approval.

If the expiration date is approaching, reach out. Since we already have your documents on hand, we can fast-track an application for an extension or a new pre-approval.

3. Are there limitations to a pre-approval?

A pre-approval is conditional and based on your circumstances at the time you apply, and it does not guarantee that the lender will approve the loan. That said, we will work with you to do everything in our power to get your finance across the line, and the pre-approval is a solid indication the lender is comfortable lending to you. If any of your circumstances change, let us know and we can discuss whether this could change your application.

Some lenders have restrictions around the type of property you can purchase and will also conduct an evaluation before the loan is approved to ensure it is satisfied with the value offered. Some limitations can include:

- Serviced apartments

- High-density properties in inner-city areas (particularly if you have less than a 20% deposit)

- Commercial or company title properties

- Properties under 50sqm

4. Does my pre-approval change if interest rates rise?

Small interest rate increases are unlikely to impact your pre-approval as the lender will take this into account as a possibility when assessing the approval. However, pre-approvals are conditional, meaning if there are major changes between getting the pre-approval and applying for the loan – such as changes to your income or interest rates increasing significantly – your borrowing power and loan application could be impacted. Because of this, it is a good idea to speak with your broker before making an offer on a property and including a finance clause in any home purchase contract.

5. I found a property I like. What next?

If you’ve found a property you believe is in your price range, it is time to make an offer. Get in touch with us first to ensure it satisfies the lender’s criteria and to receive your free property report. This report shows you the previous sales data of the property as well as recent transactions in similar properties nearby to give you an indication of what the property you like may be worth.

The way you make an offer, and the legalities around how binding the offer is, depends on the type of sale. For example, auctions are unconditional so your bid is binding. If you are asked to make an offer on a property on a contract, or your bid is accepted and you are sent the contract, speak with your solicitor or conveyancer to ensure you are satisfied with any conditions, including cooling-off periods and building and pest inspections. Even though you have pre-approval, it is usually a good idea to include around ten days for finance approval, but speak to us if you have any questions about this.

Remember to let the real estate agent know you have pre-approved finance so they know you are serious and likely able to move quickly. This can give you a competitive advantage.

6. My bid was accepted. Now what?

Congratulations! This is an exciting time, and the next few weeks will be busy to lock everything into place ready for settlement. Firstly, contact us to let us know and we can let you know what comes next.

You will usually be required to pay a deposit to secure the property. For auctions, this is often a 10% non-refundable deposit, and for other sales it can be an amount equal to 0.25% of the purchase price with the 10% balance due before your cooling off period expires. Make sure you have this deposit money ready to go or alternatively speak to us about a deposit bond, and understand what you need to do based on your contract. Your solicitor or conveyancer can help with this.

Once we have a copy of your signed contract, we will work with you and your chosen lender to get your loan formally approved and finance ready by your settlement date.

Frequently Asked Questions

Applying for pre-approval through Ingram Financial is straightforward. Get in touch with us and we’ll start by understanding your financial situation, goals, and what you’re looking to buy. From there, we’ll compare options across our panel of lenders, recommend the most suitable one for your circumstances, and manage the application on your behalf. Once submitted, approval timeframes vary by lender but can range from a few days to a couple of weeks. Getting started early – before you begin seriously inspecting properties – means you’ll be ready to move quickly when you find the right one.

While every application is a little different, most lenders will require the following:

- Proof of identity – e.g. driver’s licence and passport

- Proof of income – recent payslips (usually the last two), and your most recent group certificate (PAYG Payment summary) or tax return if you’re self-employed

- Bank statements – typically the last three months, showing your savings and regular expenses

- Details of any existing debts – including credit cards, personal loans, car loans, and their current balances

- Details of assets – savings, investments, superannuation, or any other property you own

Having these ready before we start will help speed up the process. If you’re unsure what applies to your situation, get in touch and we’ll tell you exactly what you’ll need.

In most cases, pre-approval takes between two and five business days once your application and supporting documents have been submitted. Some lenders can turn it around faster. The biggest factor affecting timing is how quickly documents can be gathered and verified. Having payslips, bank statements, and ID ready to go upfront makes the process significantly smoother. As your broker, we manage the application on your behalf and will let you know exactly what’s needed and when.

Yes, a credit enquiry is recorded when a lender formally assesses your application, and multiple enquiries in a short period can negatively impact your credit score. This is one of the key reasons to use a mortgage broker rather than applying directly with several lenders yourself. We assess your situation first and identify the most suitable lender before submitting anything, which means your credit file is only touched once. If you’re not ready to apply formally, we can also discuss your situation in general terms before any credit check is run.

Yes, though the process is slightly different. Most lenders require self-employed applicants to provide two years of tax returns and business financials to verify income, rather than the payslips a PAYG employee would supply. Some lenders offer low-doc loan options for self-employed borrowers who can’t meet the full documentation requirements, or fast track options that rely on directors wages only. The key is matching your situation to the right lender from the start. We specialise in self-employed home loans and can guide you through what each lender will want to see.

Yes. Most lenders will consider applications with a deposit as low as 5% of the purchase price, though borrowing above 80% of the property value will typically attract Lenders Mortgage Insurance (LMI). LMI is a one-off cost that protects the lender — not you — and can add several thousand dollars to the cost of your loan. Some lenders and government schemes allow eligible buyers to avoid LMI even with a smaller deposit, so it’s worth discussing your options before assuming LMI is unavoidable.

No. Pre-approval is a conditional indication that a lender is willing to lend to you based on your financial situation at the time of application. It is not a formal loan offer. Final approval is subject to the lender being satisfied with the property valuation, your circumstances remaining the same, and the loan meeting their full credit criteria. That said, a properly assessed pre-approval from a broker – rather than a quick online estimate – is a strong and reliable indicator. If anything changes between pre-approval and settlement, let us know straight away so we can reassess.

Once your offer on a property is accepted, the formal approval process begins. We submit your signed contract of sale to the lender, who will arrange a property valuation to confirm the purchase price is supported by the market. Assuming the valuation comes back satisfactory and your circumstances haven’t changed, the lender will issue formal approval — sometimes called unconditional approval. From there, loan documents are prepared and sent to your solicitor or conveyancer, who coordinates with the other party’s legal representative to arrange settlement. We stay involved throughout and keep you updated at each stage so you’re never left wondering what happens next.

Need some help?

Not sure where to start? That’s exactly what we’re here for. Drop us a message and we will get back to you within one business day with clear, honest advice tailored to your situation.